This software tour is designed to introduce you to some of the key features of ABC Focus activity based costing system. See how ABC Focus provides a structured approach to cost products, services, processes, activities and unused capacity. It provides a platform on which to confidently adjust pricing and activities for competitive advantage. A realistic estimate of the cost of products, services, customers and unused capacity is able to made quite quickly with ABC Focus.

Using an activity based costing system

Organizations need reliable costings to achieve both satisfactory margins and satisfied customers. ABC Focus software costs any product, service or process. It also has useful information to improve how the business gets things done.

How does ABC Focus work?

ABC Focus acts as a guide through the costing and margin evaluation process. It caters for both direct and indirect costs for any organization. It determines costs, margins and efficiencies.

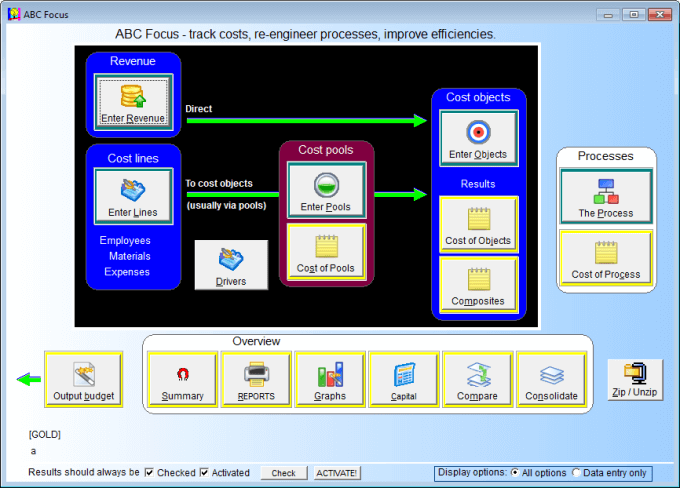

This is a new assignment so you will begin a new model. After entering a name for the new model, you see the “map” shown below.

The “map”

ABC Focus classifies the components of costing into six distinct aspects:

Items to be costed, including products and services (cost objects)

Costs of the resources – materials, expenses, and people (cost lines)

Resource usage (resource drivers)

Activities of the organization (cost pools)

Activity usage (cost drivers)

Revenue.

The costing model

Together this is known as a costing model. There can be separate models for each division or company within an organization. The main menu of ABC Focus arranges these components graphically as a map to illustrate how they interrelate. The terms can be altered in the software to suit individual business needs. Use the map (shown above) as a guide when using the software. It is a flowchart of the program.

Revenue and Cost lines

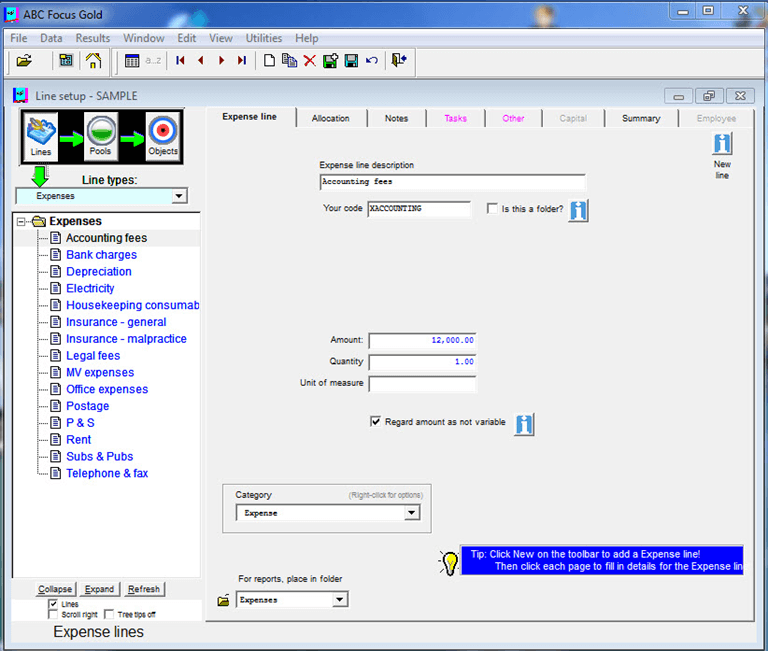

Building a model starts with entering the Revenue and Cost lines. Basically anything from which the entity incurs costs is a cost line. These costs can be broadly divided into Employees, Materials and Expenses. All are accessed from the Enter Lines button on the Map above.

Expenses cost line

The top left of the form above controls the display. You can choose between cost lines, cost pools and cost objects by clicking the appropriate icon. The green vertical arrow appears under the selected icon. You can drill down further within each section using the drop down menu’s . The choices are shown below.

Cost lines

Cost pools

Cost objects

Change the cost line to employees

Select eg nurses to show the detail of the selected line from the List tab

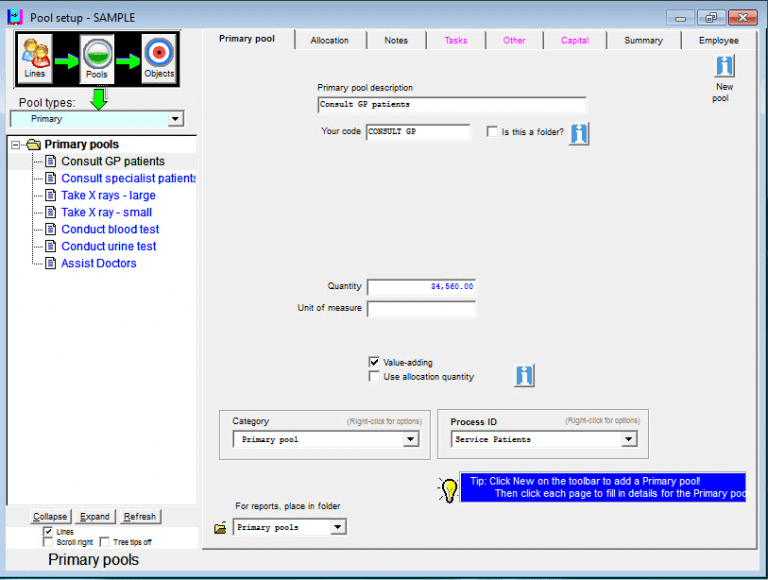

After entering expenses, employees, materials and revenue, the activity cost pools are considered.

Cost pools

The pools entered into the software are the activities or tasks performed by the organization in order to produce products or services. The activities that the business does define it – without activities there would be no business! These activities consume resources and hence incur costs. Enter the activities.

Tasks

The Tasks tab is used to enter more detail about any of the activities. For example, there may be an activity called: Telephone and reception. The relevant employee might spend time doing a host of different tasks like

Administration

Manage reception

Maintain car park roster

Receive and send faxes

Direct email messages to appropriate persons

Maintain staff phone list

Open incoming mail/sort and distribute

Receive visitors

Attending to taxi hire and flight bookings

Filing

These would all be entered under Tasks.

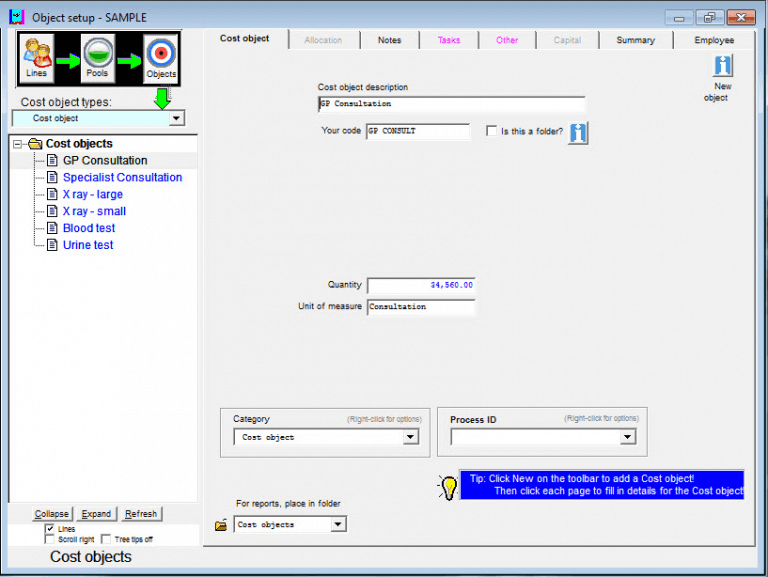

Cost objects

Any item or activity that you want to cost is a “cost object”. This is the final destination of all costs and revenues. Cost objects are usually products or services, but they can be used to accumulate cost and margin data for analysis of anything such as markets, clients and sales campaigns. In the example below we wish to determine what the cost is to the practice every time a blood test or urine test etc is done.

Resource and cost drivers. Allocate cost lines to pools and objects

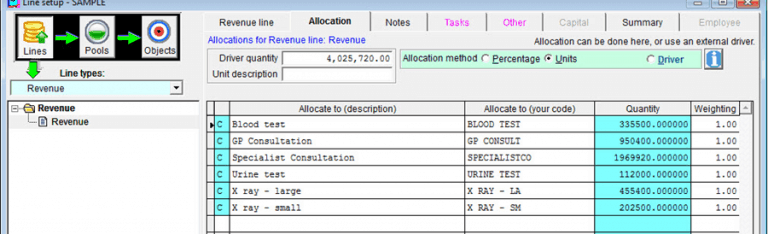

Having entered the revenue, employees, materials, expenses and the activities that the business does, you are ready to finalize the costing model by entering the allocations. First allocate the revenue.

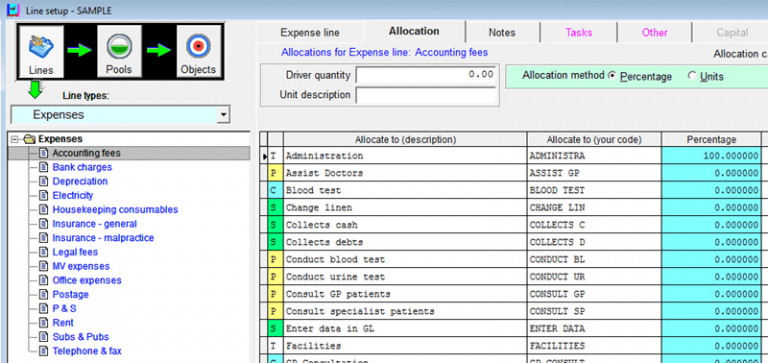

Allocate expenses

Now allocate the expenses. For example 100% of accounting fees is allocated to Administration

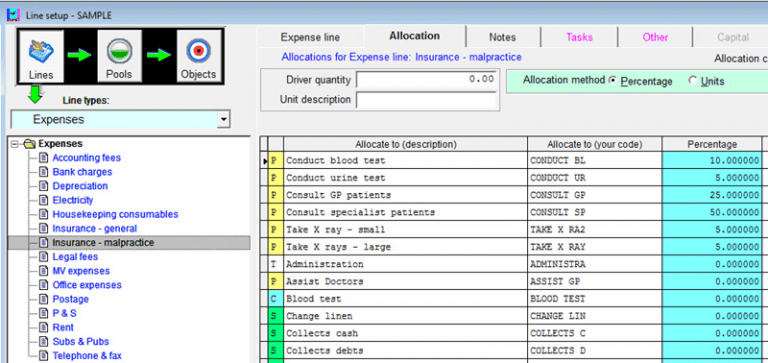

Another expense example: The cost of malpractice insurance is allocated by percentage to a number of cost pools

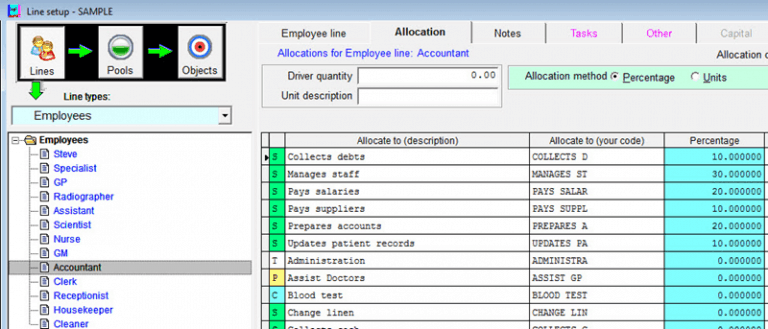

Allocate employees

After allocating the expenses, the employees are next. Here the accountants time is allocated to different activities

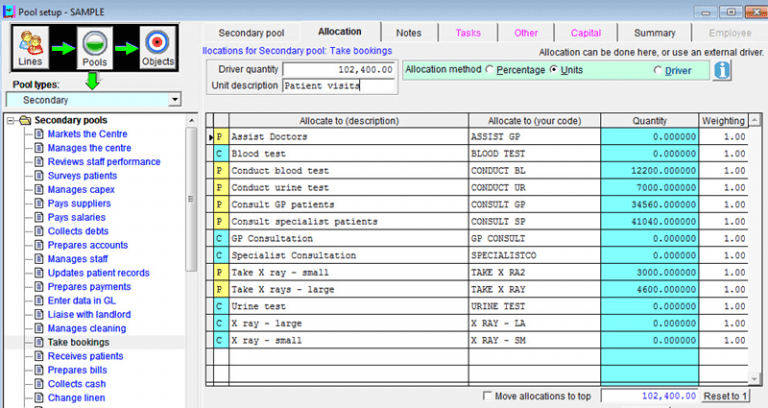

Drivers for cost pools

Finally, appropriate drivers are selected for each activity cost pool. For example, there may be a cost pool to do with deliveries. An appropriate driver could be the number of deliveries made.

The software makes it easy to enter the drivers. Here is an example:

A cost driver called patient visits is entered into the software.

The patient visits driver is assigned to one or several activity cost pools. For the medical center example they have activity cost pools called Take bookings and Collect payments that depend on the number of patient visits. So the “patient visits” driver entered above is assigned to them.

Often the initial driver will be an estimate – the figures can be improved over time. Doing the costing exercise will reveal where more detail is required and this can be added into the model as required.

The job is done. It’s now time to let ABC Focus do its work.

See the results

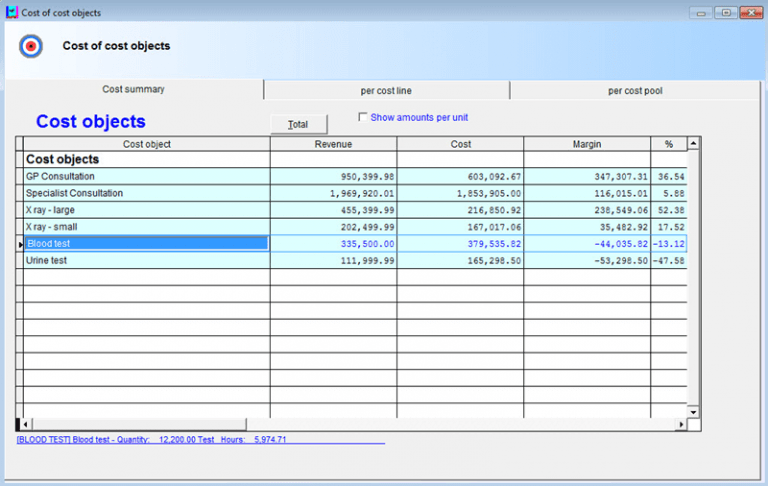

So what do things cost?

The software shows the results in a report or conveniently on the screen

What this costing model tells us

This organization was surprised to see that they charge less for blood tests than it costs them.

Furthermore, the margin on specialist consultations is less than on their general practitioner consultations. Some of their products are profitable, some are losing them money.

Analyse the cost

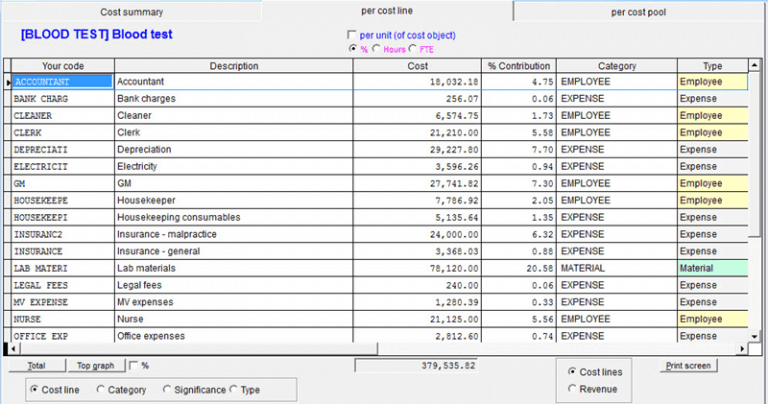

The software is excellent at analyzing the costs; can things be done better or differently to make the problematic products and services more profitable? Use ABC Focus to find out:

This shows the components of the costs in order of significance.

Now the team can get their thinking hats on to see what can be done.

Can the scientist do more tests? Is new technology available to make it cheaper?

Cost components in significance order

Tracking the costs backwards from the cost object to the cost line gives another important perspective on cost components of cost objects

Reverse track costs

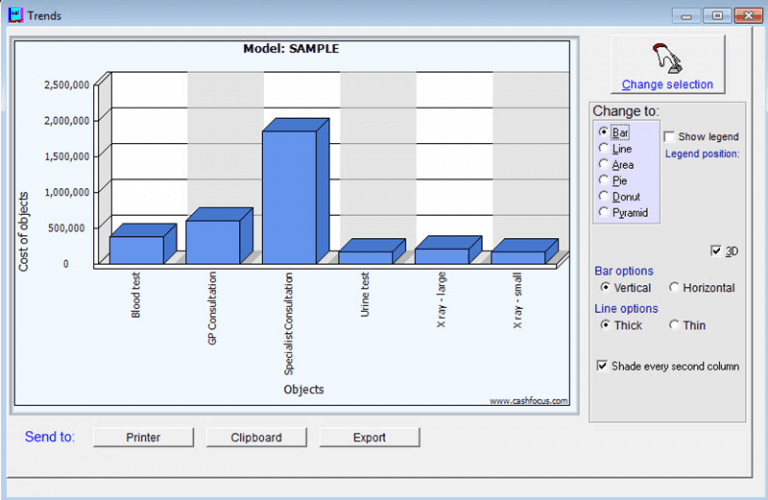

Graphs

Look at the contribution or margin of products and services graphically:

Budgets reports as graphs

Reports

The software includes extensive reporting, graphing and tree analysis capabilities.

Other advanced features

Capital is able to be integrated into the ABC Focus model. ABC Focus includes capital costs.

ABC Focus provides all the benefits of output based budgeting.

ABC Focus monitors costs every month, and compares costs month to month.

ABC Focus costs processes as well as activities.

Share the data

Portability

There are a number of ways to facilitate model transfers between locations.

Zip/unzip models

Data can be compressed into a .zip file or retrieved from one. This functionality adds convenience to model mobility with your costings. You may want to save and retrieve models from alternative selected locations possibly for backup purposes or to send a model to someone electronically. Whatever the reason, for these occasions the Zip and Unzip functions are built in to simplify the task and optionally reduce the file size of the model which is handy for electronic transfer.

Export budgets

Reports can be printed or exported to Excel, Word and PDF. Costings can be imported or exported from any system that has the ability to export / import data to an Excel or ASCII formatted file.

Conclusion

Comprehensive costing tool

ABC Focus is a tool for costing any product or service. It caters for both direct and indirect costs.

If your organization wants to cost services, products or activities for successful business management and for business improvement then ABC Focus is the tool to use. It will guide you through every step from entering the employees, materials, expenses and revenue through to determining the costs of the products, services and activities and evaluating the margins.